Is Buying Land a Good Investment?

Does land make a good investment?

Whether for a future homesite or commercial endeavor, owning land is a fantasy we’ve all had at one point or another; land is clay waiting for our sculpting hands.

But land is arguably the most intimidating real estate endeavor, quite simply because it requires more work and has more unknowns than the average buyer is looking to inherit. Land in already desirable areas is also very scarce, which means a lot of land investing requires you to see value where others don’t, be right about it over time, and justify the economics behind your ideas. These are big (ok, enormous) undertakings for an average buyer unless they’re already equipped with a talented real estate broker, tax professional, and financial planner.

In today’s post, I’m going to discuss a few critical elements to review while looking for your ideal piece of land. But as you’re reading, keep in mind that land investing is extremely risky and requires a massive due diligence process that exceeds the details discussed here.

Establish Attractiveness

The first thing to do with any land plot is to evaluate the overall feeling you get from the land. Read your instincts and be mindful of your optimism. Drive out there, walk the property twice, smell and look around; is this the one?

Next, ask some basic questions. For example:

Can I afford it?

How easy is it to access the land?

Do I like the location?

What else is nearby?

Do the neighbors look respectful?

How flat is the land?

Is this land elevated or depressed relative to its surroundings?

What is the soil like?

Does the city protect the wildlife here?

Is this on a wetland or near a major body of water?

What are the current taxes?

The list above is by no means exhaustive, but it does offer some relevant questions to make sure any further research is worth the effort.

Easements

Easements are physical, and sometimes unmarked, sections carved out of your property that you cannot develop because they are reserved for other resources, such as utilities or sidewalks. For example, most properties have a boundary along the property that you cannot build upon, usually somewhere between 10ft to 30ft. To make sure your easements are accurate, you need to review the property survey. Older surveys may lack the required details, so getting an updated survey can often be a critical contingency in your offer.

Some properties include easements for utilities, which renders the land unbuildable and/or requires the utility company unrestricted access to those portions of your lot. For example, power lines may run through your backyard or portions of your land could be sequestered for drainage. In the image below, those large dotted circles are drainage areas that can’t be built upon and the smaller solid circles (T9-T13) are protected trees that can’t be removed.

Utilities and MUDs

Speaking of easements, access to utilities is another consideration. Here some thought questions:

Water: Do I need to dig a well to get water? Not all properties have access to city water.

Sewage: Do I need a septic system? A septic tank is found in households that aren't served by municipal sewers.

Electricity: How will the property be served by electricity?

Are the property taxes reflecting additional costs for utility access via municipality utility districts (MUDs)?

MUDs are projects that build utilities with borrowed funds; the bonds are paid down by homeowners via property tax assessments. Because MUDs are funded via debt and are shared by all respective homeowners, assessments will vary over time according to property values and remaining debt levels.

Zoning

Each city has zoning restrictions, which define the allowed activity on the lot. Zoning is important because it protects you from both neighbors and developers. For example, it would be financially devastating to buy a single family home only to see a developer come in and start tearing down nearby homes to build an RV park; this is but one of many horror stories my real estate broker has shared with me!

Zoning varies by location, but will typically be defined like this:

No Zoning

Single Family Homes (large or small)

Multi-family Homes (low, moderate, or high density)

Commercial office

Light industrial

Major industrial

Mixed use

Agricultural

Historic

Each zoning type has pros and cons. For example, you can’t convert a single family home to a duplex to make revenue. Likewise, you’ll have difficulty modifying historically zoned sites because they’re highly regulated by the respective city.

Deed Restrictions

Deed restrictions are covenants that define what a homeowner can and cannot do; they are more specific and nuanced than zoning restrictions.

Restrictions can be a blessing in disguise by shielding you from neighbors who do things that destroy property values. Many deeds restrict the use of firearms, fireworks, animal agriculture, junk collection, and commercial operations. This gives you protection from a neighbor who suddenly decides that running a commercial pig farm or noisy scrap yard in their backyard is an A+ idea.

Some neighborhood restrictions can be a headache though. For example, if your goal is to build a second home for your aging parents, a restriction may prevent the use of a second structure and/or mobile home from sitting on the lot. Likewise, some covenants may restrict your ability to raise a few chickens in the backyard, even though your enterprise is small and has no profit motive.

Ultimately, the most important point is to make sure that the property you’re purchasing doesn’t have deed restrictions that invalidate your intended use while also protecting you from bad neighbors.

Nearby Properties

Nearby properties tell you a lot about how much you’ll enjoy your land and what sort of resale price it may have in the future. Any pre-existing structures as well as easements, zoning, and deed restrictions of nearby properties can help you assess the quality of the land you’re researching.

Proceed with caution when you see such things as:

Train tracks: Noise, even late at night.

Commercial operations: Pollution, water contamination, loud noises, and nauseating smells.

Rivers and streams: Increases the risk of flooding

Unsightly neighbors: Dumping trash or leaving rusted, broken down cars in their front yard.

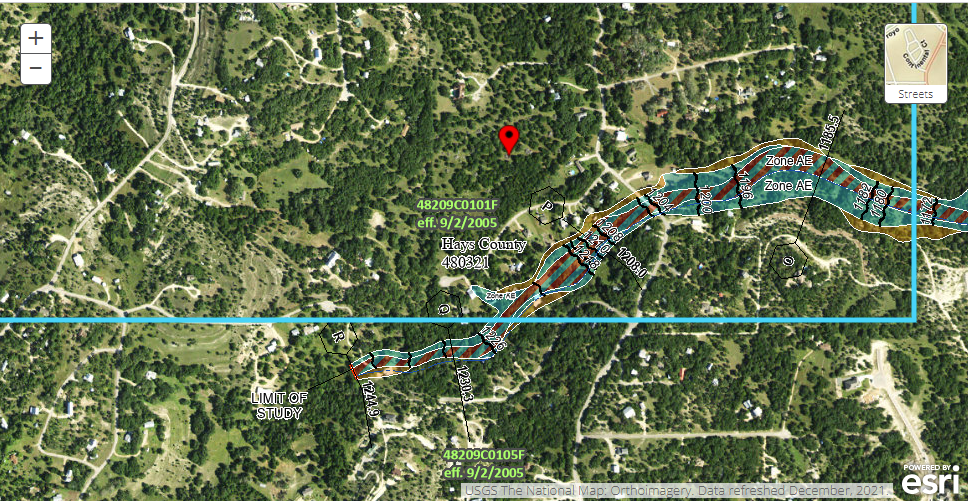

Floodplains

Over 50% of homes flooded by Hurricane Harvey were outside of 100-year floodplains. While it may not be uncommon for a 5+ acre lot to have a small area where flooding may occur, it’s extremely important you understand your intended development and make sure the price you’re paying is worth it relative to the flood risk. FEMA has flood maps you can find here.

Being in a floodplain will also increase your flood insurance premium rates.

The floodplain of nearby properties should also be explored. Nearby rivers and streams may increase the risk of flooding. A smaller but still possible risk is that a neighbor develops (or has already developed) their land such that it diverts more water to your property than your research would indicate.

Building Costs

If you intend to build on your lot, the costs of land clearing, utility connection, building materials, and labor may change your plans dramatically. As build costs soar to $275-$300 per square foot in 2022, the economics of buying land to build make less and less sense. In addition, cities often require builders to do uneconomical things, such as getting permits, planting trees, or building drainage structures due to landscape modifications.

The overall point I’m trying to make here is that land is about much more than just the price you pay. You need to factor in all the extra costs that come with it to bring your idea to life.

Land Loans

Because land represents a greater risk to a lender than a home mortgage, land loans are significantly more expensive:

Monthly payments are determined based on a 20-year amortization schedule with a final balloon payment due in the 10th year.

Interest rates are typically 1% to 2% higher than a home mortgage and have adjustable rates.

A land loan isn’t necessarily a deal breaker, but it’s important to recognize that a lender is really pushing you to develop the land because that brings down their risk dramatically. When you do acquire additional funds to develop the land, you’ll incur additional fees to refinance the land loan. Cash closing the land and using financing for your homesite or commercial development project reduces financing charges; albeit, it requires much large funding upfront.

Closing Thoughts

Hopefully this mini guide was helpful to put some context around the sort of tasks required to buy a piece of land. It’s impossible to take every risk off the table, but there is a huge amount that can be done to lay the foundations for successful land investing. As mentioned earlier, working closely with a team consisting of a real estate broker, tax professional, and financial planner is essential to making the most of your capital resources.